Listen to this Museletter

From Ancient Alchemy to Modern Frontiers

For centuries, materials have dictated the pace of human progress. Bronze gave way to iron, steel built cities, and silicon sparked the digital revolution. But every great leap forward wasn’t just about discovery—it was about timing, scalability, and economic advantage. Today, we stand at another frontier: engineered materials designed at the atomic level, capable of reshaping energy, technology, and even global power dynamics.

Key Data Points Driving the Shift

- Lithium demand is set to grow 9x by 2040, but 60% of global supply is controlled by just three countries—Australia, Chile, and China—creating critical vulnerabilities.

- China refines 90% of the world’s rare earth elements (REEs), essential for EV motors, wind turbines, and semiconductors, making supply chains highly fragile.

- Sodium-ion batteries, a lithium-free alternative, are projected for mass adoption by 2025, offering a cheaper and geopolitically stable solution for energy storage.

- Graphene—200x stronger than steel and a breakthrough for next-gen electronics—remains limited by high production costs, but commercialisation is expected within a decade.

This edition of The Agna Museletter examines how novel materials reshape industries and energy, focusing on factors driving material adoption, supply chain vulnerabilities, and the dominance of specific nations like China in critical material refining. It provides a framework for investors, policymakers, and industry leaders to navigate the evolving materials landscape and anticipate future shifts.

Museletter Highlights:

- Agna Insights

Explore how novel materials are reshaping energy, technology, and global industries - Agna Perspectives

Interesting and insightful reads from our social media - Team Activity

Collaborations, engagements, and interactions with key players in the DeepTech ecosystem - On the ‘Front’ier Tech

Latest updates on Frontier Technologies - Agna Recommends

Team Agna’s curated recommendations for you

Agna Insights

Note: Novel Materials & Energy isn’t just about innovation—it’s about impact. Investors can spot the next big breakthroughs, policymakers must act on resource security, and founders have a world of untapped potential waiting to be built.

Introduction: Materials that Define Eras

Some materials don’t just support progress—they define it. Steel built modern cities, reshaping skylines and industries. Silicon shrank computers from room-sized machines to pocket-sized devices. These materials didn’t just refine technology; they unlocked entirely new frontiers. But why them? Why did silicon revolutionise computing while others faded into obscurity? Understanding this distinction matters. It reveals how discoveries transition from interesting concepts to indispensable foundations of industries, economies, and daily life. By studying what made these materials transformative, we can better predict which innovations today will shape the future.

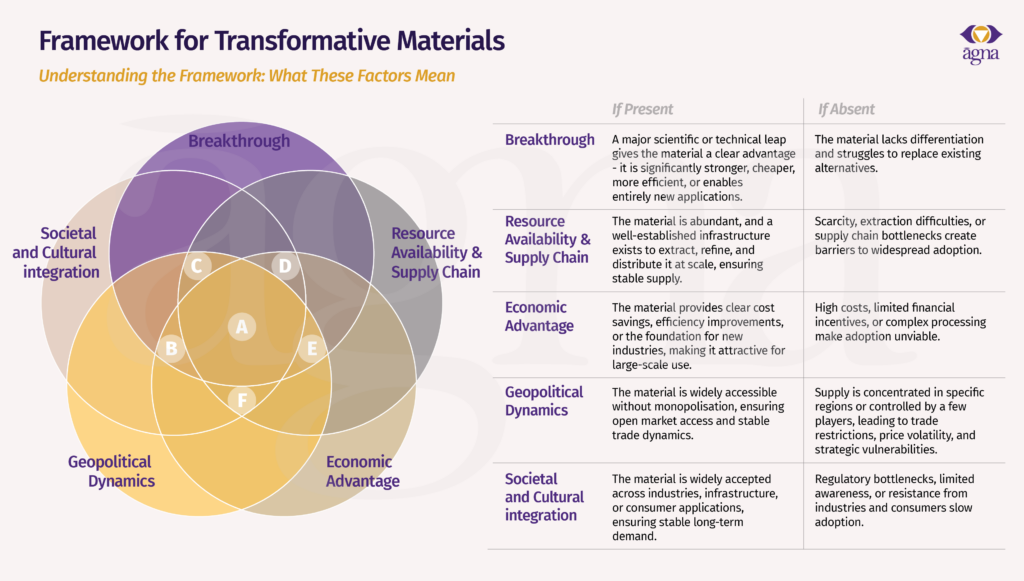

The Materials That Matter: What Drives Widespread Adoption?

History shows that the adoption of materials follows clear, recurring patterns. Five key factors drive this process, and their convergence determines whether a material becomes widely adopted:

The framework helps us assess how different forces shape adoption paths. The following scenarios (non-exhaustive) illustrate how variations in these factors determine whether a material thrives or remains limited:

A – Total Adoption → Widespread Industry Transformation: When all factors align, the material becomes deeply integrated into global industries and supply chains.

Effect: It drives economic growth, geopolitical dominance, and unlocks entirely new industries.

B – Scarcity Dominant → Power Concentration & Market Disruptions: Control is centralised, leading to price volatility, monopolisation, and accelerated R&D into alternatives.

Effect: Those controlling access gain influence, while industries face instability and push for substitutes.

C – Weak Economic Advantage → Niche Adoption & Slow Growth: High costs and limited financial incentives delay adoption despite technological promise.

Effect: The material remains confined to specialised use cases, struggling to scale commercially.

D – Geopolitical Blockage → Trade Restrictions & Supply Instability: Regionalisation and political tensions limit access, forcing nations to secure alternative supply chains.

Effect: Countries invest in domestic production or pivot to substitutes, increasing costs and uncertainty.

E – Low Societal Integration → Resistance & Limited Market Penetration: Regulatory, cultural, or usability challenges prevent widespread acceptance.

Effect: The material fails to reach mass markets, restricting its impact to specific industries.

F – Infrastructure Deficit → Stalled Commercialisation & Unrealised Potential: Manufacturing, logistics, or supply chain gaps prevent scaling, even if the material is viable.

Effect: Adoption slows, industries delay usage, and more accessible alternatives take priority.

Through the Material Lens: History of Materials and Power

Every major material that reshaped history did so because it aligned—or failed to align—with these five factors. Few sparked revolutions, while others remained limited until conditions shifted.

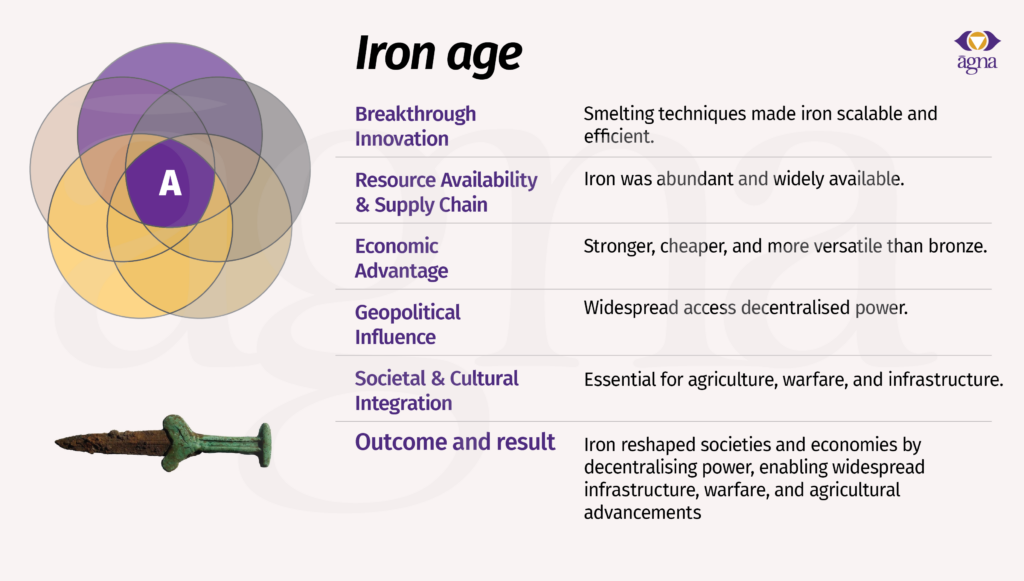

Iron → The Material That Built Civilisations:

Abundant and scalable, iron replaced bronze, decentralising power and driving economic expansion. Enabled military dominance, infrastructure development, and long-term civilisational stability.

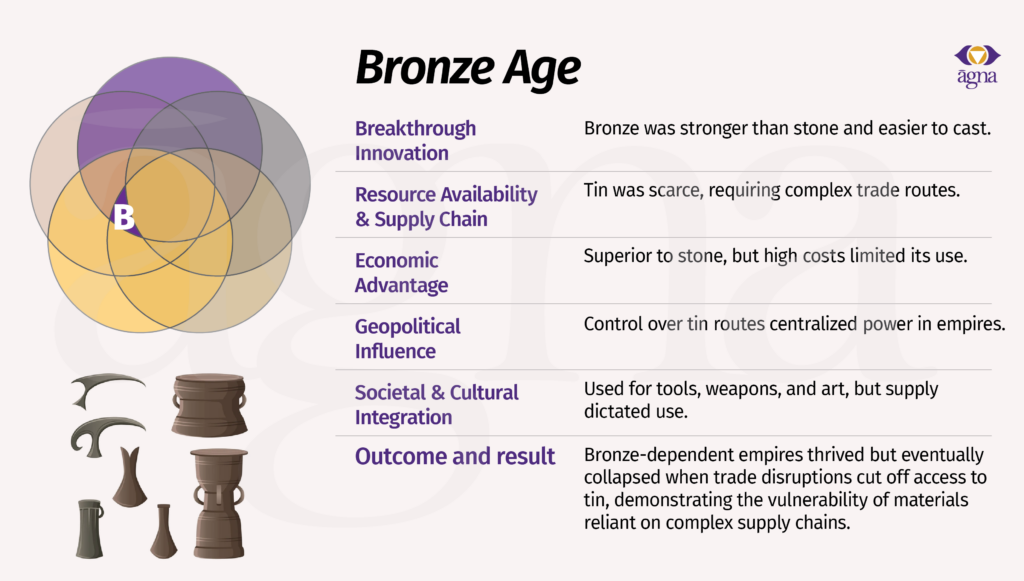

Bronze → Strength with a Supply Chain Problem:

Superior to stone, but dependent on scarce tin, making societies vulnerable to supply disruptions. Early empires controlled the tin trade, but when routes collapsed, bronze-dependent civilisations declined—much like today’s semiconductor shortages.

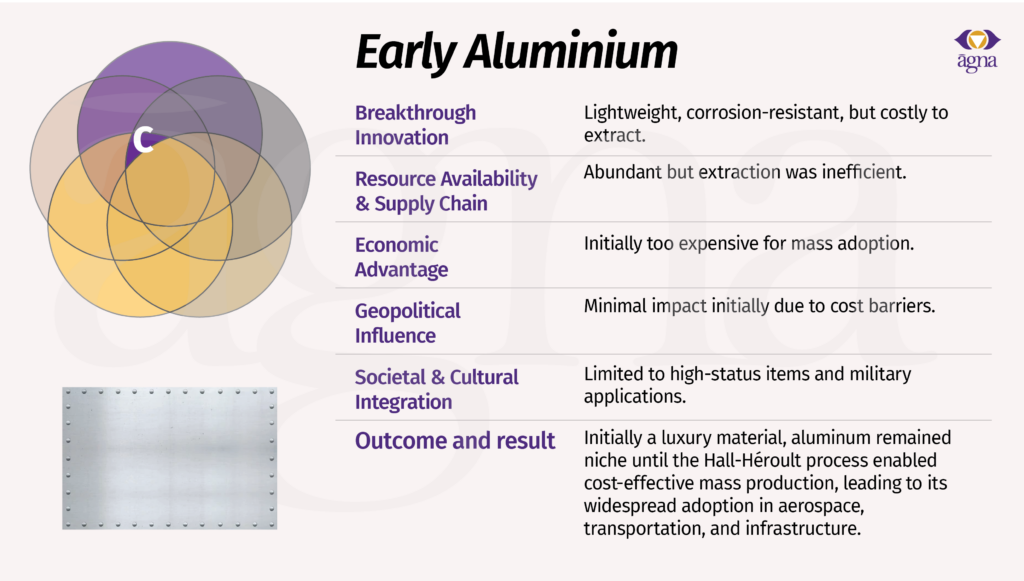

Aluminium → A Breakthrough That Took Time:

Lightweight and strong, but early production was expensive, limiting adoption. The Hall-Héroult process (1886) made it affordable. Once costs dropped, aluminium revolutionised aerospace, transportation, and construction.

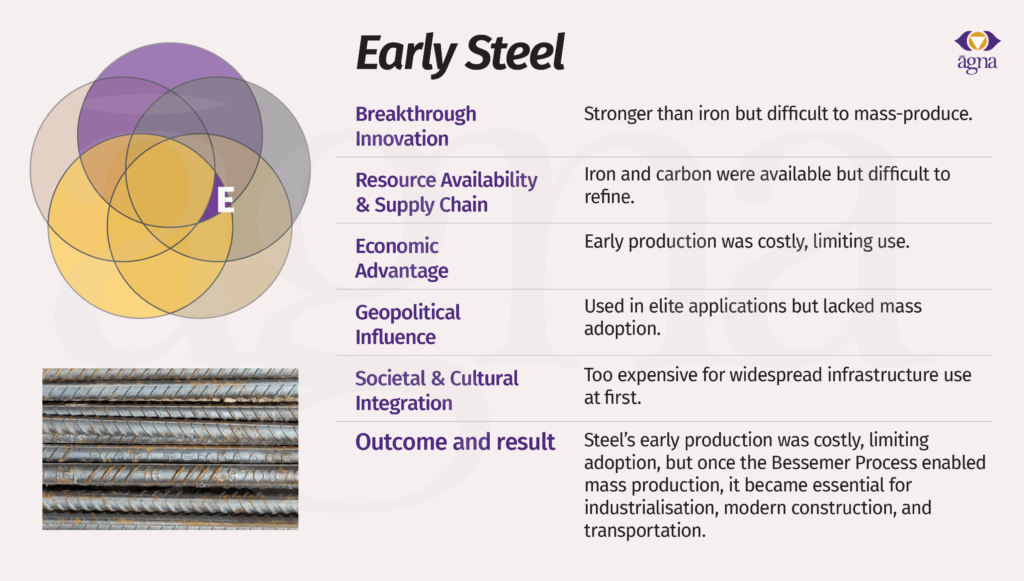

Steel → The Right Process at the Right Time:

Stronger than iron but initially costly. The Bessemer Process (1856) enabled mass production. Aligned with industrial needs, driving the growth of railroads, skyscrapers, and global infrastructure.

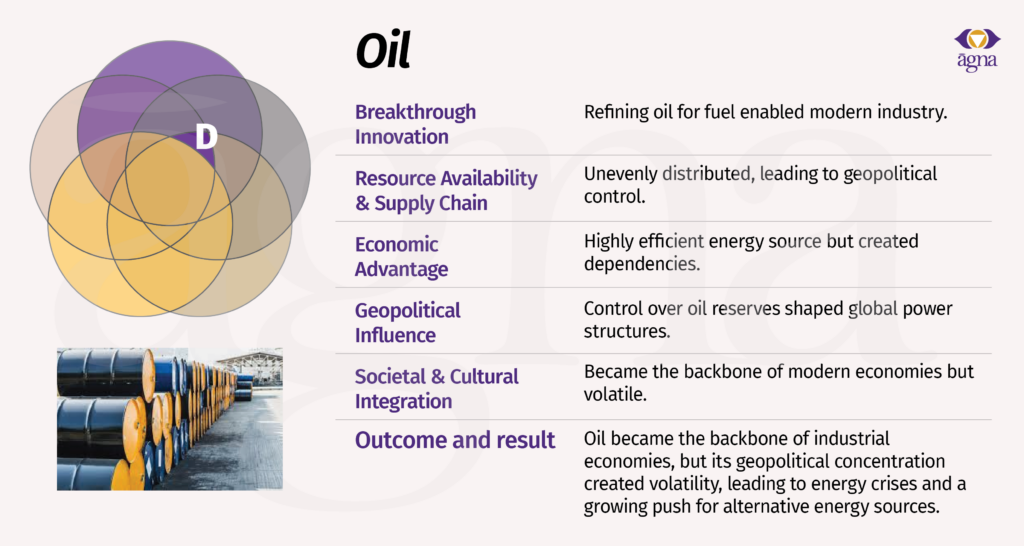

Oil → A Resource That Reshaped Global Power:

Essential for industry and transportation, but concentrated reserves created geopolitical leverage. The 1973 Oil Crisis showed the risks of resource dependency, pushing nations to seek alternatives for energy security.

Concrete → A Material That Stalled Without Infrastructure:

Roman concrete enabled durable infrastructure but disappeared for centuries after Rome’s fall. Without sustained production capabilities, its potential remained unrealised until modern rediscovery.

Materials as Catalysts for Change

Today, we stand at a similar inflection point. Lithium, cobalt, nickel, uranium, and graphite form the backbone of energy storage, electrification, advanced manufacturing, and nuclear energy generation. But just as bronze fell due to supply constraints and cobalt is now fading due to cost and ethical concerns, these materials face mounting pressures—geopolitical tensions, economic volatility, and the relentless push for alternatives. The question is not just which materials are in demand today, but which will endure. Using the five-factor framework, we can dissect their long-term viability—identifying those that will dominate, those that will decline, and the forces that will shape their trajectory.

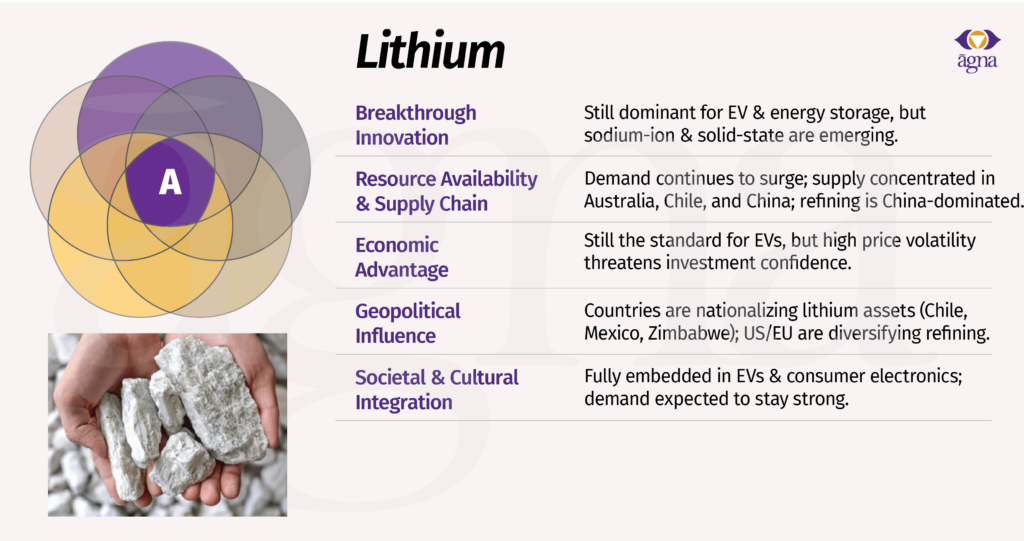

Lithium: Indispensable but Under Pressure

Lithium remains the backbone of modern energy storage, with demand projected to grow 9x by 2040 due to the EV boom and grid-scale storage expansion.

Despite this, lithium’s future is shaped by three key challenges: extreme price volatility, supply chain concentration, and emerging battery alternatives such as sodium-ion and solid-state technologies. While Australia and Chile dominate mining, China controls over 70% of refining capacity, making it a strategic geopolitical asset. Western economies are scrambling to onshore refining and recycling to reduce dependency. The near-term supply landscape is fragile—lithium prices fell 75% in 2023, deterring new investments, yet supply is still expected to tighten by 2030 due to surging demand. Recycling and alternative chemistries will grow, but lithium-ion remains dominant for at least another decade.

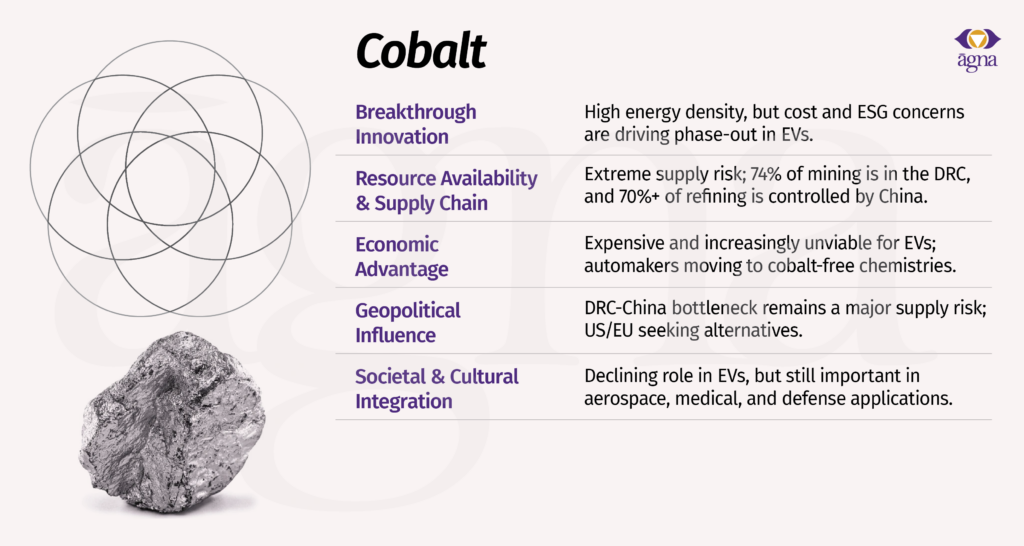

Cobalt: In Structural Decline

Historically crucial for battery stability and energy density, cobalt is now being engineered out of mainstream battery chemistries due to high costs, ESG concerns, and geopolitical risks.

Over 70% of cobalt supply originates from the DRC, where political instability and ethical concerns (child labor, unsafe mining) have driven automakers and battery manufacturers to shift toward cobalt-free solutions like LFP (lithium iron phosphate) and high-nickel cathodes. China dominates refining (~80%), making cobalt a geopolitical flashpoint, particularly as Western governments seek alternative sources (Canada, Australia, Indonesia). Despite a structural decline in battery use, cobalt remains critical for aerospace alloys, medical implants, and high-performance magnets. Over time, recycling and technological advancements will further displace its role in mainstream energy storage.

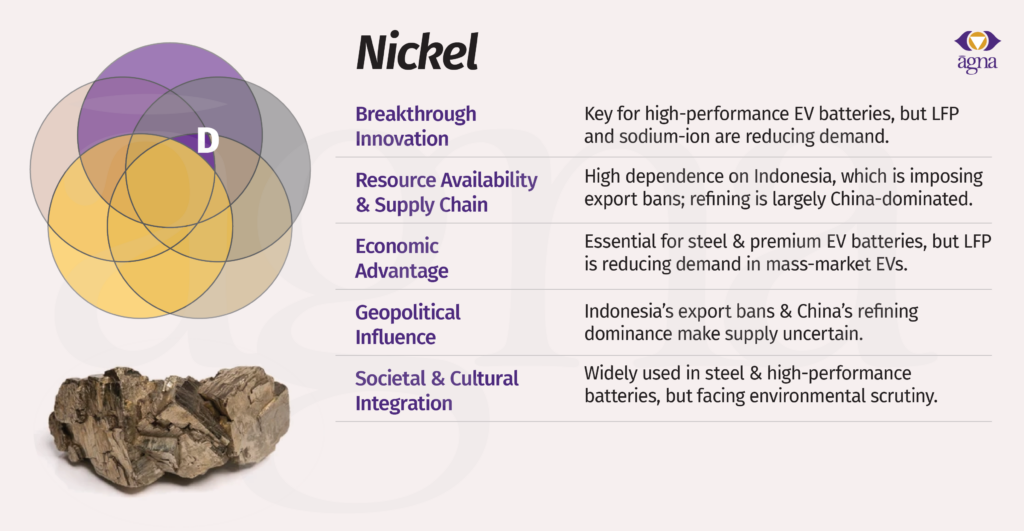

Nickel: Premium but Facing Substitution

Nickel is essential for stainless steel, aerospace, and high-energy-density EV batteries, but faces an uncertain future in energy storage.

While high-nickel cathodes (NMC, NCA) enable longer-range EVs, the rise of LFP batteries—which do not require nickel—is reshaping demand. Indonesia, the largest producer, is strategically leveraging its supply, imposing export bans and refining mandates to force domestic processing. China’s dominance in nickel refining (~70%) mirrors its control over lithium and cobalt, creating geopolitical risk. Meanwhile, Russia (Norilsk Nickel) supplies ~7% of global nickel, adding another layer of uncertainty amid global tensions. Nickel will remain crucial for premium EVs and industrial applications, but its role in mainstream energy storage may diminish over the next decade as LFP adoption accelerates.

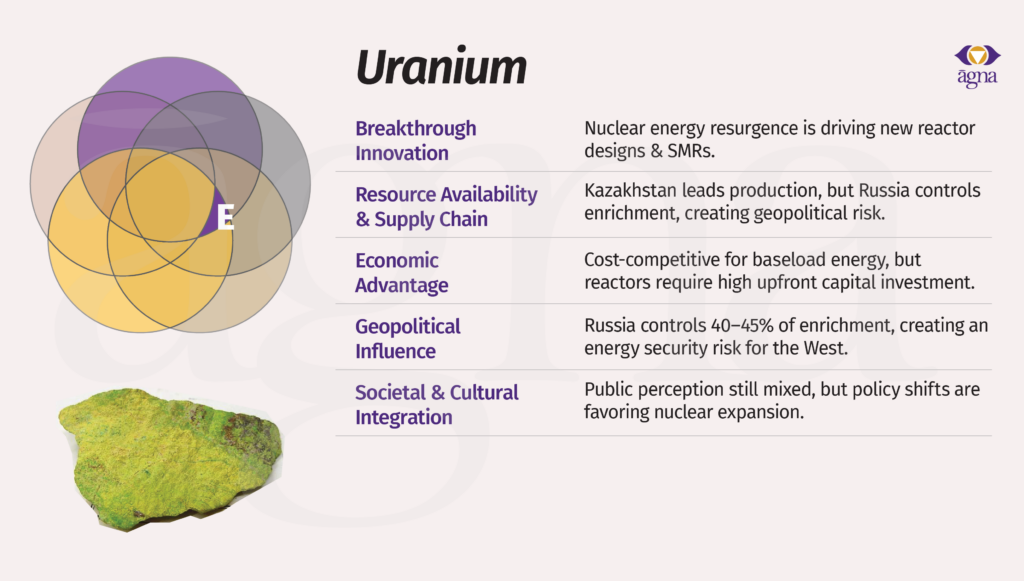

Uranium: The Key to Nuclear Energy’s Future

Uranium is experiencing a resurgence, as global energy security concerns and decarbonisation efforts drive renewed interest in nuclear power.

The small modular reactor (SMR) revolution and long-term reactor expansions have pushed uranium demand higher, with prices surging ~250% from 2021-2024. However, the uranium market remains highly geopolitically sensitive—Kazakhstan (~43% of supply) dominates mining, while Russia controls ~45% of global uranium enrichment. The U.S. and Europe are now scrambling to rebuild domestic uranium processing capabilities to reduce reliance on Russian-controlled supply chains. Nuclear energy adoption is growing, particularly in China, India, and the Middle East, but the industry remains constrained by high capital costs, regulatory hurdles, and persistent public skepticism. If geopolitical shifts continue, uranium’s resurgence will be met with increased investment in Uranium alternatives.

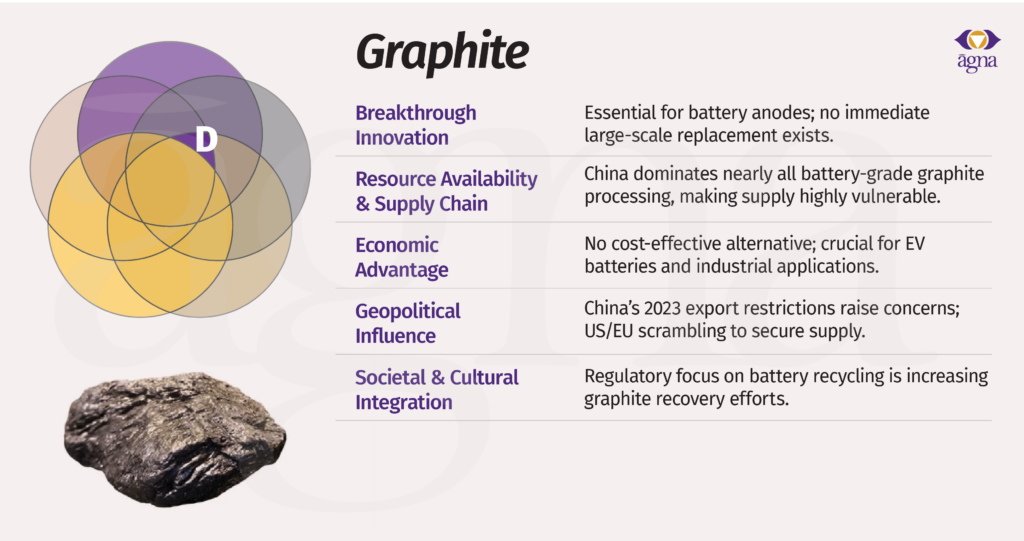

Graphite: The Underestimated Supply Risk

Graphite is often overshadowed by lithium and cobalt, but it is a foundational component of lithium-ion batteries, comprising over 70% of battery anodes by weight.

Unlike lithium, graphite is not rare, but its supply chain is overwhelmingly controlled by China (~78%), making it a geopolitical bottleneck. In October 2023, China imposed export restrictions on battery-grade graphite, raising concerns about supply security for Western EV manufacturers. Governments and automakers are now investing in alternative sources in Canada, the U.S., and Africa, while synthetic graphite and recycling are gaining traction. Graphite demand is expected to grow 4-5x by 2035, but the real challenge is scaling non-Chinese processing capacity. Unless new refining hubs emerge, graphite could become a major chokepoint in battery supply chains.

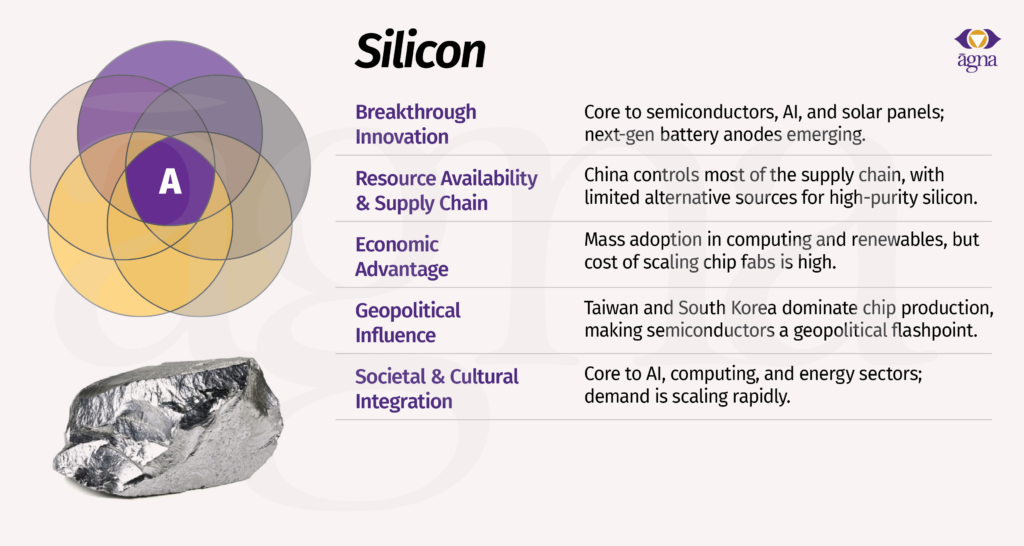

Silicon: The Backbone of Electronics & Solar Energy

Silicon is indispensable for semiconductors and solar panels, making it one of the most strategically important materials today.

Over 90% of solar panels and nearly all computer chips depend on high-purity silicon, yet China controls ~75% of polysilicon refining. Recent U.S. and EU export controls on semiconductor technologies have intensified geopolitical tensions, leading to reshoring efforts in chip manufacturing (Intel, TSMC, Samsung expanding U.S./EU fabs). For solar energy, polysilicon demand is skyrocketing, with solar installations growing at a record pace (~300 GW in 2023). However, an oversupply of polysilicon has driven prices down, challenging Western producers. Silicon’s role in global technology is unquestioned, but its supply chain will be increasingly shaped by geopolitical realignments and sustainability concerns.

End Note: A Universal Framework for Material Exploration

As we move forward, understanding how materials evolve—from discovery to dominance to potential obsolescence—is essential for those shaping the future of industry and innovation. The framework outlined in this edition applies across any material class—whether foundational to modern life, emerging through scientific breakthroughs, or yet to be fully commercialised. This structured approach provides a lens for investors, policymakers, and founders to anticipate shifts in material demand, identify bottlenecks, and position themselves strategically.

- For investors, it helps assess market potential, supply chain risks, and long-term scalability of critical materials, enabling differentiation between short-lived trends and sustainable, high-growth opportunities.

- For policymakers, it offers a structured way to anticipate resource constraints, supply dependencies, and strategic vulnerabilities, informing decisions on industrial incentives, supply chain resilience, and national security strategies.

- For founders and industry leaders, it highlights the key factors that dictate adoption and integration into global markets, helping refine go-to-market strategies, mitigate supply risks, and position new materials or technologies for scalable adoption.

TLDR;

- Material adoption follows a predictable pattern—

Breakthrough innovation, Resource availability & supply chain, Economic advantage, Geopolitical influence and Societal & cultural integration- that determines whether a material scales globally or remains niche. - Lithium remains critical but volatile—

with demand projected to grow 9x by 2040, its supply chain remains fragile, as China controls 70% of refining and price swings deter long-term investments. - Cobalt is being phased out, while nickel’s role in EVs is shrinking—ethical concerns and supply risks (70% from the DRC) drive automakers toward cobalt-free batteries, while LFP adoption threatens nickel’s demand.

- China dominates critical material supply chains—

78% of graphite, 75% of polysilicon, and 80% of cobalt refining are under its control, raising concerns over resource security and triggering diversification efforts. - Uranium demand is rising amid energy security concerns—

with prices surging 250% since 2021, nations are racing to reduce dependence on Russia’s 45% control over uranium enrichment, reshaping the nuclear energy landscape.

Agna Perspective

- Scientists at Max Planck have discovered that topological chiral crystals can accelerate water splitting for hydrogen production by 200 times, marking a major breakthrough in clean energy.

- Life sciences are set to reach a $13.89B market by 2034, with AI-driven breakthroughs already accelerating R&D, enhancing efficiency, and transforming the industry.

- India’s Union Budget 2025 allocates ₹2,000 crore ($240M) to expand the IndiaAI Mission, a 1056% increase from last year, driving AI integration in key sectors like agriculture, life sciences, and industry.

Team Engagement

Team Agna at Step Dubai 2025, connecting with startups, investors, and industry leaders to discuss AI, sustainability, and the future of technology.

With the Middle East emerging as a key hub in the East-West Corridor, Agna is committed to building that bridge.

On the ‘Front’ier Tech:

- Scientists have developed hydrogel-coated surfaces that mimic natural joints, achieving superlubricity and offering a sustainable alternative to traditional lubricants.

- As the first wave of solar panels nears the end of its lifespan, innovations in recycling—like laser-based separation and salt-etching—are making solar energy more sustainable than ever.

- Researchers have developed a graphene-based solar absorber with a three-layer design—aluminum, indium antimonide, and silver—achieving up to 97% efficiency across broad wavelengths, significantly enhancing solar thermal applications.

Agna Recommends:

Energy: A Beginner’s Guide by Vaclav Smil

provides a clear, concise introduction to the science, history, and future of energy, explaining its fundamental role in shaping civilisation.

Power Trip: The Story of Energy by Michael E. Webber

explores how energy has driven human progress throughout history, shaping economies, politics, and daily life.

A Question of Power: Electricity and the Wealth of Nations by Robert Bryce

examines how access to electricity determines economic prosperity, global inequality, and the future of energy security.

Listen to this Museletter

Questions? Feedback? Different perspective?

We invite you to engage with us and collaborate.

Warm Regards,

Team Agna

Click below to join our mailing list for The Agna Museletter.